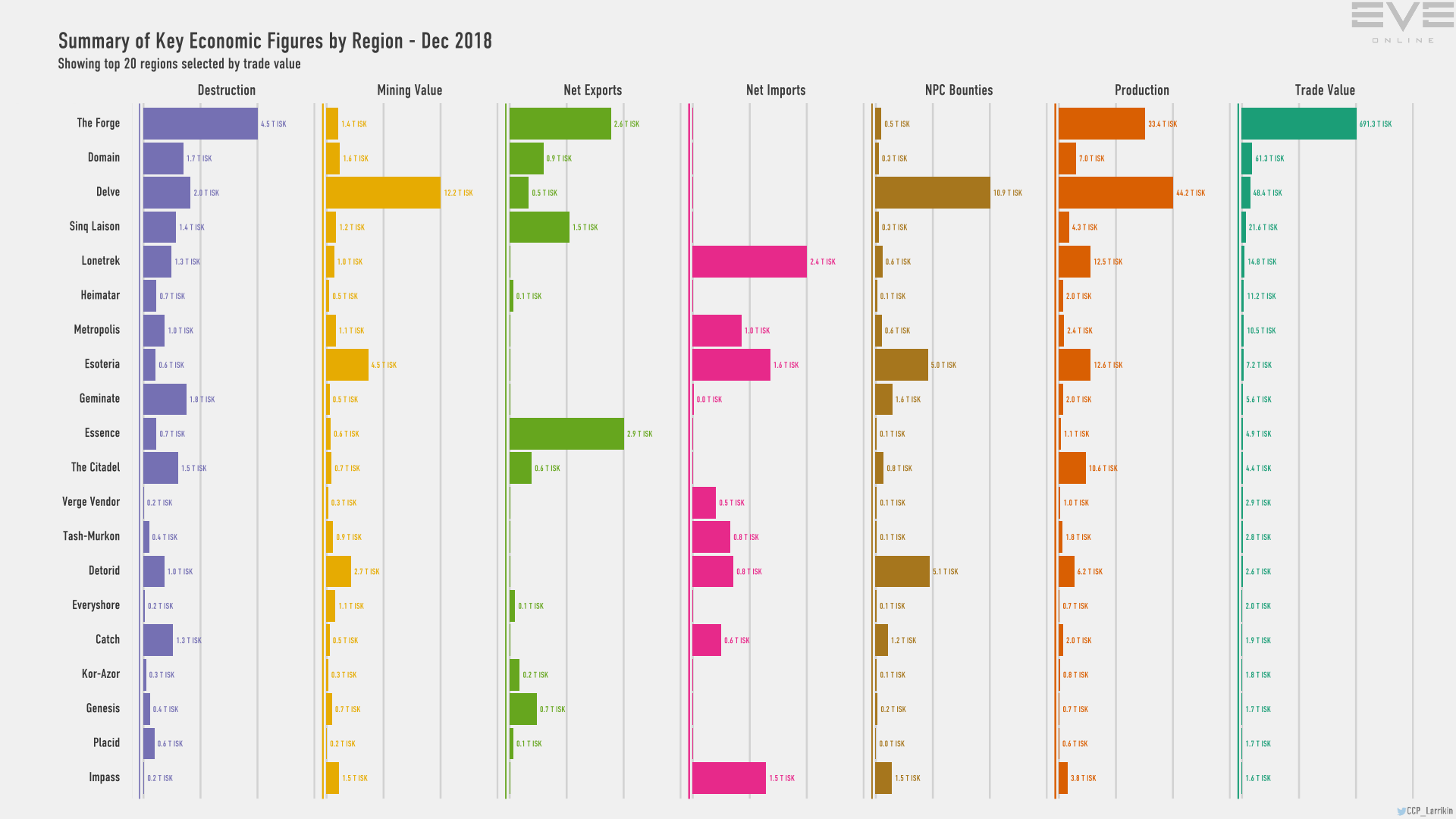

Indeed, but… to me, more interesting to compare the overall mining / bounty balance between the 4 empires. Not a huge surprise that Amarr (the biggest) area wins at mining, but Caldari (the most populous, thanks to Jita and so many Caldari created toons as a result of it) wins at bounties.

Heck, Minmatar was ALMOST ahead of Amarr in total bounties despite being way behind in mining. And on that note, despite being last in bounties, Gallente was slightly ahead of Caldari in mining to grab the #2 spot there.

With the smallest region and probably the smallest pop, Minmatar comes in last on mining… but managed 3rd in bounties ahead of Gallente, so well done to them on that!

These figures are generated by looking at the value of everything that passes through the region border. This includes things like supercapital fleets. This if someone had their fleet in essence at 0:00 on the 1st December and jumped it elsewhere at some point thereafter, that would count as a massive export for the month of December. I’m not saying that is what happened here for sure , but I feel that it’s a likely explanation.

Win-win.

Alliances will improve their logistics (only alliance that can manage logistics, can hold space and move fleets through multiple jumps with reasonable speed), collapse their stretched holdings (holding space you can’t control is taxing), move significant portion of production into their territory (it’s no longer feasible to bring everything from Jita), and the metagame inducing factor (the “jump fatigue” stupidity) is also removed.

In the first chart the first red circle is when the growth in the money supply went bonkers and CCP stepped in and in short order proposed some rather draconian nerfs to carriers and super carriers. The second red circle is what is happening lately. As we can see there is an increase in the ISK supply that is on par with what we saw from Mid April of 2018 that elicited a response from CCP. In December we see an almost similar increase in the ISK supply and…nothing.

The second chart shows the day-over-day change in the ISK supply. The first red circle is May 5th and is the largest daily change in the ISK supply with a 13 trillion ISK increase on just that day alone. In December we saw 3 days (the 11th, 12th and 15th) where the ISK Supply increased by 8, 9.47 and 9.51 trillion ISK respectively. For December alone the ISK supply increased 80 trillion (the data covers 30 days). Starting in April 12th and going for 30 days (the time frame around when CCP noticed the sudden surge in the ISK supply and decided to nerf carriers and super carriers) we saw an increase of approximately 93 trillion ISK.

What are you talking about? Yeah, I’ve been very critical of the idea that the money supply was growing too fast…and generally that was the case. Primarily because if the money supply grows “too fast”–i.e. faster than the real economy–you get inflation. But we have not observed inflation. But this growth has been quite rapid in the money supply and when looking at the real economy growth there has been downwards. This is a situation where if real growth does not start to pick up soon with this level of growth in the money supply we are looking at an increased inflation. And in looking at the CPI that is exactly what we are starting to see. The money supply started to grow in November. Real output started to decline in November and the CPI is going up since November.

Fortunately it looks like in January there was a large negative active ISK delta that has actually reduced the size of the money supply…

I think the rapid growth in money supply is caused by the development of these newcomer alliances like test,winter co and ph.And their growth in consumer power actually cancelled the effect of increasing money supply.

That negative isk delta either is bot/rmt money or has had no impact on the market for the last three months though.

Since those are the two main criteria by which we get negative active isk.

Which means in either case its probably not a major market driver.

{kind=link}